Difficulty

Difficulty

You've probably noticed that you have to pay more and more money for routine purchases. Times of high inflation are not pleasant for our wallets, as the amount of goods and services we can buy with the money in our accounts is decreasing (money is losing its purchasing power).

However, similar to stock market downturns or economic recessions, periods of high inflation are something we have experienced before, represent a natural part of the economic cycle, and can be defended against.

Our new series will attempt to present a comprehensive guide on how to approach the current economic situation from the perspective of an ordinary person managing their personal finance. You will learn the answers to questions such as:

- What is inflation, and why is it currently so high?

- How long will it stay?

- What groups of people will be most affected?

- How will it affect our income (whether at working age or retirement)?

- How will it affect our savings and debts?

- How do we set our long-term financial strategy to ensure we are protected?

What Even Is Inflation?

Inflation is the increase in the general price level of goods and services in an economy. In the media, we encounter it as a percentage, called the inflation rate. Statisticians track this variable by observing changes in price indices. The best-known (and most important for us) is the consumer price index (CPI).

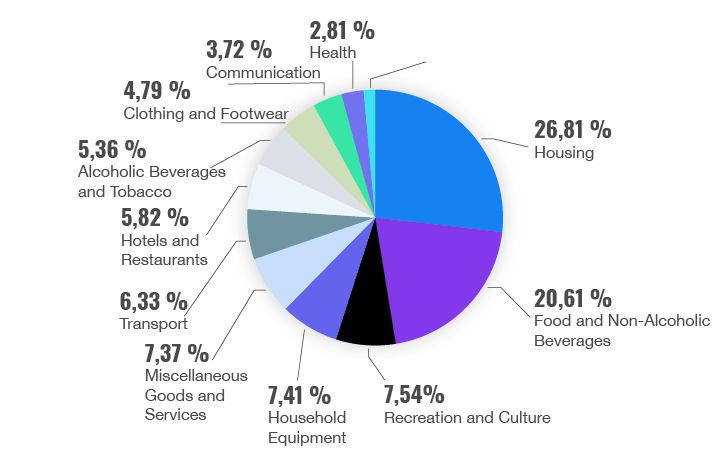

Simply put, it is the shopping basket of goods and services that a typical household buys each month. The largest items in it have the highest weight (if a typical household spends 30% of its income on rent, it will represent 30% of the basket).

The chart below depicts the current distribution of goods in the Slovak consumer basket. We can also construct price indices for other groups if, for example, we seek to track the purchases of typical producers. However, these are more important for economists than for ordinary people.

Every month, the Statistical Office collects data on the prices of these goods and calculates the total price of our shopping basket. If its purchase cost rises compared to the same month in the previous year, we are experiencing inflation. And that is happening throughout the Western world these days.

In April 2022, consumer prices in Slovakia rose by 11.8% compared to the previous April. Other countries are also dealing with inflation. The latest data from the US speaks of 8.3% inflation, the Eurozone recorded a price increase of 7.4% year-on-year in April.

Source: Statistical Office of the Slovak Republic

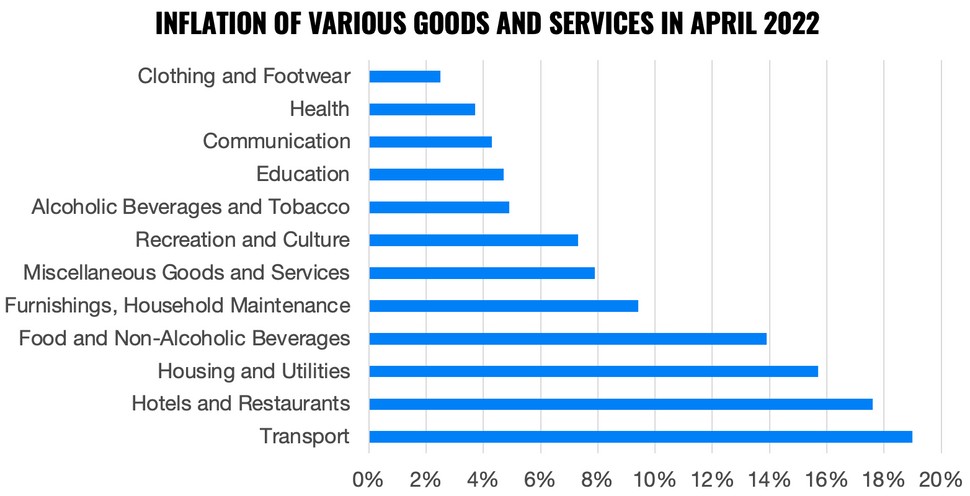

Inflation is a weighted average, with the prices of different goods and services rising at different rates. The chart above shows which items have seen the most significant rise in their price tags over the past year. Contrarily, it reveals which sectors have not been affected by inflation as much.

The sad fact is that essential goods such as rent, energy, food, and fuel have incurred the hardest inflationary hit. In contrast, the services sector (except for restaurants and hotels) hasn’t been affected that much.

One inaccuracy of this measurement method is that it ignores the possibility of immediate substitution, i.e., the adjustment of purchases to price changes. For example, if the figures in your local restaurant’s menu rise faster than groceries from the store, you are likely to limit eating out, cooking more often at home instead.

Hence, the distribution of the budget will change slightly compared to the original basket. Inflation, therefore, tends to overestimate the real increase in the cost of living.

What causes inflation?

Rapid price increases generally arise for two reasons. The first is an increase in demand for goods and services. Whenever people's purchasing appetite exceeds the ability of firms to produce at the same rate, producers start charging higher prices for their output.

Take an example: if 200 people flock to a car dealership that has only 100 cars on offer, the sellers can easily raise prices as they will still be able to sell everything. This type is called demand-pull inflation.

The second type is cost-push inflation. This occurs when inputs needed by most firms for production suddenly get more expensive. A popular example is a rise in the price of oil, which pushes up fuel and energy prices.

Since all firms use these (from transporting goods to heating the office), most producers will see their costs rise. To avoid making a loss, they will pass the increased costs on to consumers in the form of higher prices for goods and services.

Why Has It Arisen?

The current inflation wave is a mix of both types. One side of it is a broken supply. The pandemic has quarantined key ports and bankrupted firms in supply chains, causing shortages of imported goods.

Combine it with the shortage of chips (used to make laptops or cars), which were already getting out of stock before the pandemic, and the quarantine measures have made things worse. The invasion of Ukraine was the imaginary nail in the coffin, as the war sent energy and commodity prices soaring, driving costs further up.

In addition to a reduced ability to supply the market with goods, people's willingness to spend has also increased. For several years, loans were available at near-zero interest rates. Households have accumulated savings during the pandemic, as services such as restaurants and cinemas were closed, leaving us with few spending opportunities. This triggered a shopping spree when restrictions were relaxed.

Over the past few years, both the stock market and property prices have risen, making many households feel richer. This has also fuelled their appetite to splurge on goods and services.

These reasons make it clear that inflation is not just a Slovak problem but plagues all Western countries. Instead of waiting for politicians to save the day (they cannot do much beyond limited supportive benefits), it is, therefore, better to take the situation into our own hands.

How Long Will It Stay?

The honest answer: no one knows. It depends on the military developments, the sanctions, the growth of interest rates and wages. All those variables cannot be accurately predicted. Most analysts currently think that inflation will rise in the coming months, slowing down in 2023 and 2024.

There are several reasons for such predictions. Interest rates will have risen by then, making borrowing more expensive and naturally depressing demand. Households will run out of savings accumulated during lockdowns and buying enthusiasm will cool off. European countries will try to secure more reliable energy suppliers than Russia, which would bring the price down.

The most important lesson, however, is that it does not matter at all. This blog series seeks to demonstrate that with sensible long-term management of personal finance, short-term inflationary shocks pose no problem. Hence, they aren’t worth speculations or unnecessary fear.

Where to Store Wealth in Times of High Inflation?

In our communications, we have long stressed that there is no need to panic in economic crises and market downturns. The best thing to do is to simply keep buying shares regularly or make an extra deposit if you have savings for this purpose. High inflation is similar to market downturns. It is a temporary condition, and the best response is not to react to it at all.

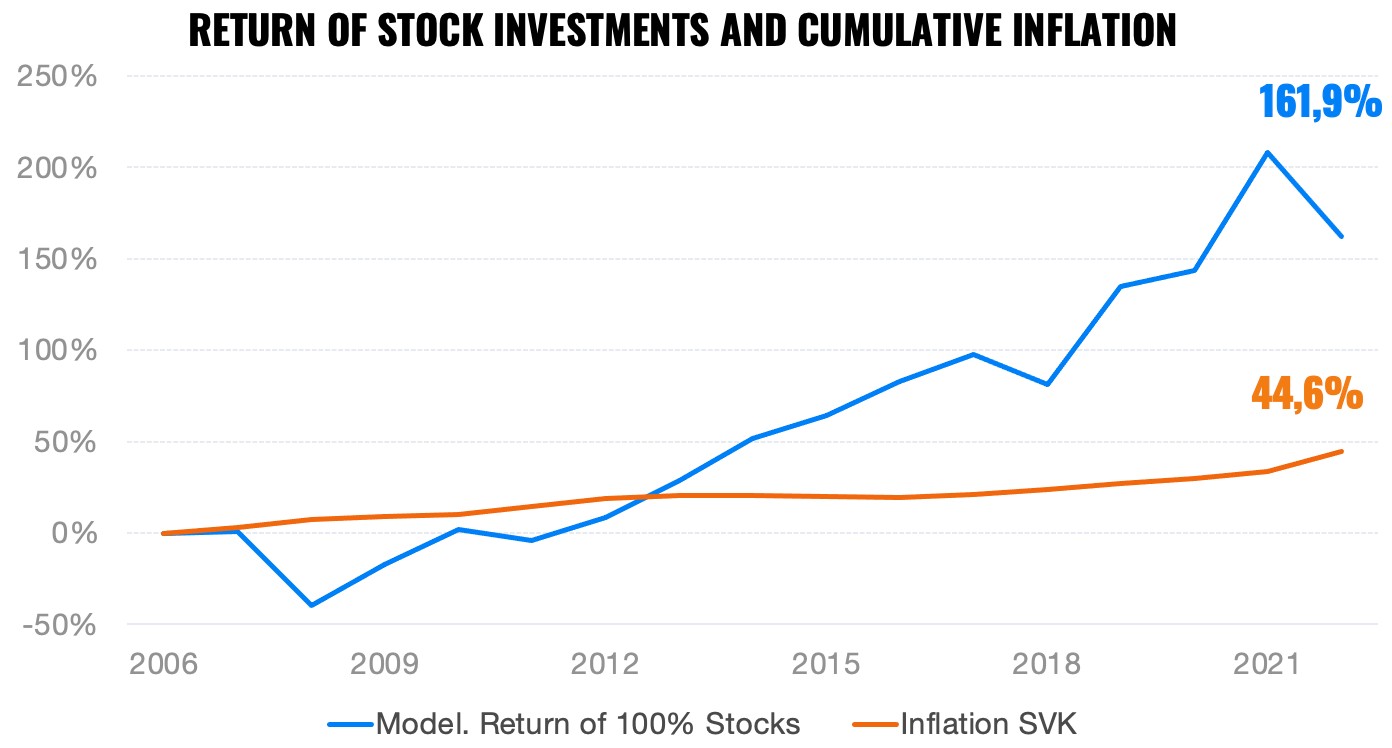

Historical data shows that stock markets rise faster than the price level over the long term. Lifelong investing will easily shield us from inflation. It is good to build up savings and an emergency fund for short-term waves of price rises.

Yes, stock markets or bond portfolio prices may fall temporarily. But if you invest for 20 or 30 years, you'll barely notice this challenging period on the chart of final returns, almost certainly earning good returns.

Shield your wealth via long-term investing.

If you're at the beginning of your investing journey (like many of our younger clients), work with long-term data when setting your lifelong financial strategy. If you develop an aversion to stocks or bonds just because inflation beats them in one year, you could be setting yourself up to lose a lot of money over the next few decades.

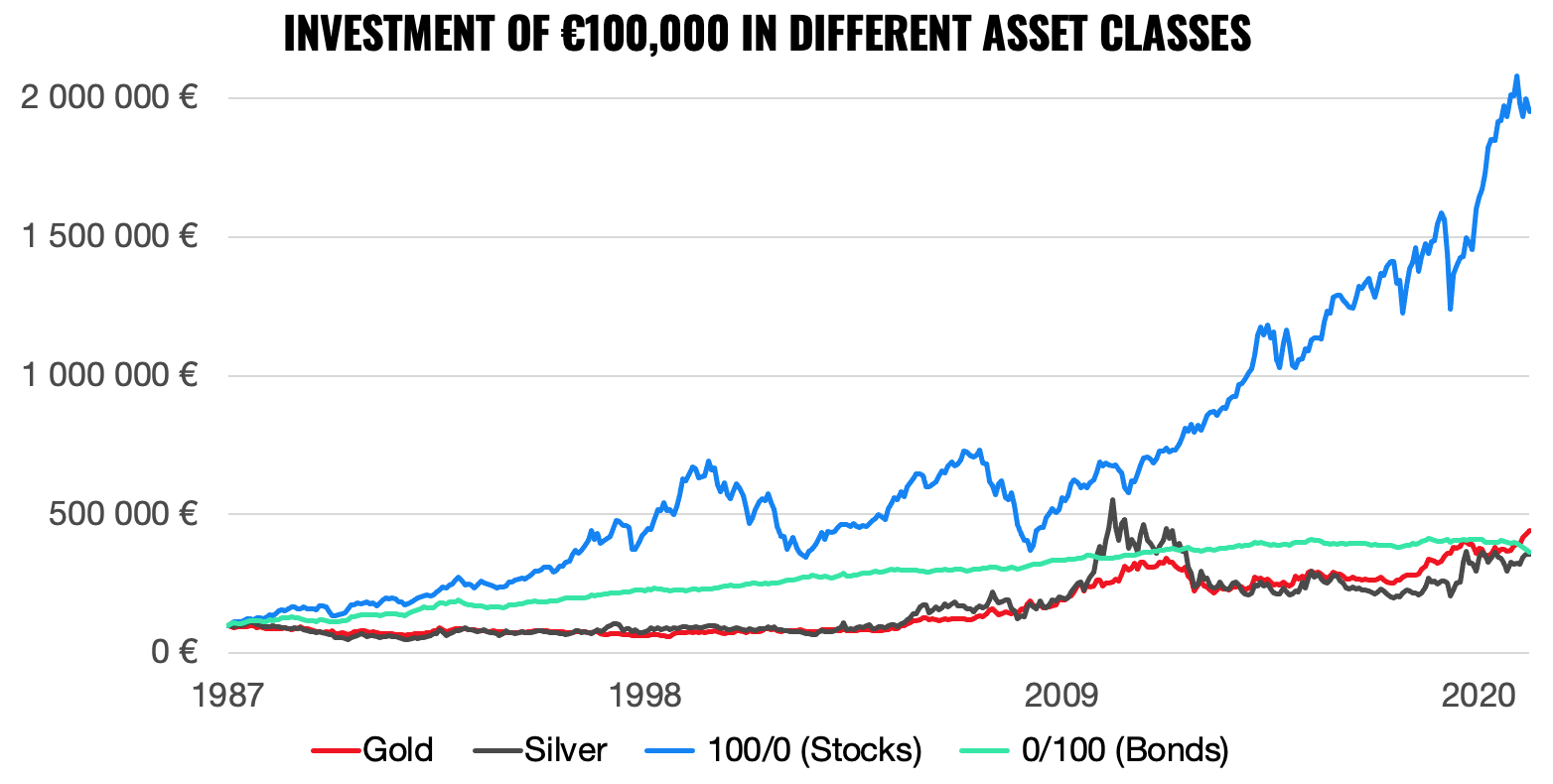

In the chart above, you can see the development of the value of investments in several asset classes from 1987 to April 2022 (two of which represent the modeled results of the portfolios we offer in Finax). You can see that gold and silver experience sharp increases in certain periods. Those are mostly times of high inflation or market downturns.

Investors like to flee into precious metals in uncertain times, as their value is tied to the physical stock. Hence, they should be theoretically protected from suddenly falling along with the markets (that's why they’re also called real assets). Investors entering the markets during inflationary periods may gain the misconception that it pays to prefer these assets.

However, it is clear from the chart that stocks and bonds tend to gain faster in all other periods, while commodities have been stagnant over the long term. Even if they manage to jump in the short term, they soon fall back, erasing the preceding inflation-protection effect. You’d need a crystal ball to predict this peak. It's impossible.

Trying to sell at the exact commodity peak would be more akin to gambling. Hence, to reliably build decent wealth, it pays to have the bulk of your portfolio invested in productive assets like stocks and bonds. Don't be fooled by periods when they don't do well. Just hang in there and ideally keep buying at sale prices.

Who Will Be Threatened by Inflation and Who Will Gain?

Although it may sound strange at first, inflation does not have a noticeable impact on all population groups. Some people will benefit from it. We will split the analysis into three age groups: the young, the middle-aged, and pensioners (or people drawing an annuity).

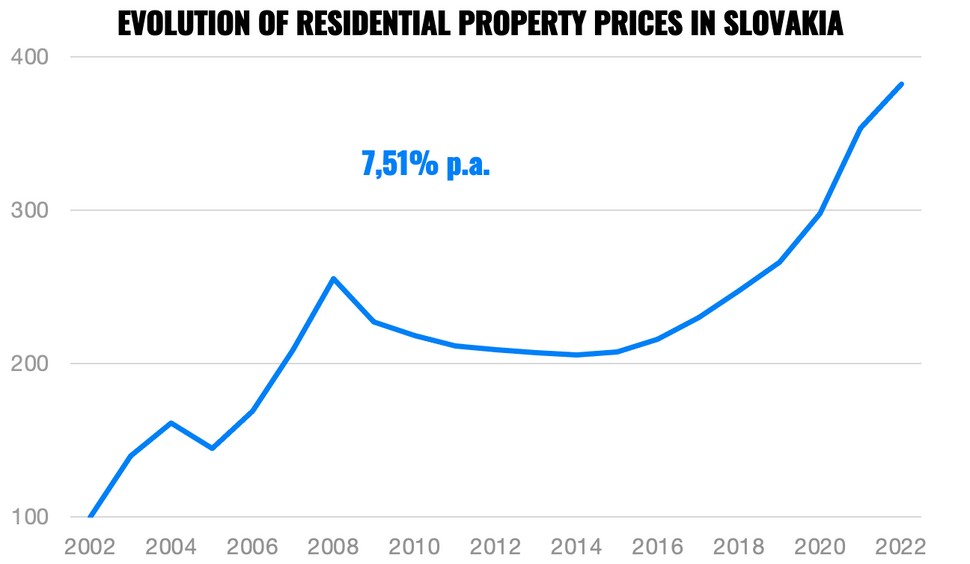

Young people will be affected by inflation if they are still planning to buy their own homes. Both property prices and the cost of money (interest rates) are almost double what they were a few years ago. However, if they have already purchased real estate, inflation will help them.

Loose monetary policy enabled them to obtain loans with favorable interest rates that are fixed for the upcoming period (3, 5, or 10 or more years). As the rising price level reduces the purchasing power of money, they pay back less valuable money than they borrowed.

Hence, they get a generous discount on their first home, as they’ll give up less purchasing power over the whole repayment period compared to a scenario without inflation.

The young also don't have to worry much about high prices. Job offers usually reflect inflation with higher starting wages. Coupled with career advancement and productivity growth, their salaries should rise more than the general price level in the next few years.

As far as middle-aged people are concerned, unfortunately, inflation will hit low-income households the hardest. The essential goods whose prices have risen sharply take up a larger proportion of their budgets compared to high-income households. The latter spend more on services that are less affected by inflation and don’t represent necessary expenses.

However, this does not mean that low-income households are powerless. In the next parts of the series, we will discuss in detail the impact on income, debt, and savings, explaining several mechanisms by which even low-income households can defend themselves.

State pension recipients will be hurt by inflation if their spending rises above the level of their pension this year. Benefits paid from the first pillar are adjusted for inflation, but with a significant delay. Each January, pensions rise by a percentage of pensioner inflation for the first half of the previous year.

Since current inflation did not start until the second half of 2021, pensions only rose by 1.3% in January. However, the situation should turn around next year, with pension growth anticipated to outstrip the rate of inflation.

The government is correctly considering responding with an extra early rise in pensions this year to help vulnerable pensioners offset significantly higher prices.

Moreover, pensioner inflation is measured using a different consumption basket that is more typical for retirees. If goods that have low weights in it (e.g. fuel) become more expensive, then pension increases may not reflect this.

A Brief Concluding Teaser

We hope that this overview has helped you get your bearings on the current situation, its reasons, and its implications. Soon we will publish two more blogs that will focus on the impact of inflation in three spheres of personal finance: income, debt, and savings.

Each will include detailed advice on how to protect yourself if you belong to a group negatively affected by inflation.