Difficulty

Difficulty

Despite the fact that there has been a lot of media coverage and the TV stations have covered this topic heavily in their newscasts, let's briefly summarise what actually happened before we get into some recommendations for clients.

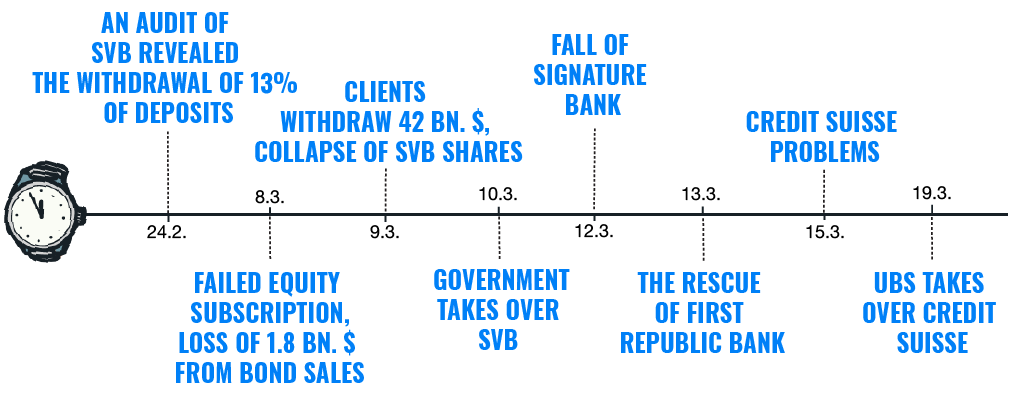

February 24 - Silicon Valley Bank's (SVB) audit has been signed by KPMG, with 13% of all deposits leaving the bank since the end of the first quarter of 2022, which has had a negative impact on the bank.

March 8 - SVB announced a $1.8 billion loss on the sale of Treasury bonds after the stock markets closed to cover increased customer withdrawals. The bank used the deposits to buy US Treasury bonds, which fell in price due to rising interest rates. Without collateral, the bank was losing money.

9 March - Bank shares experience a huge fall. They lost $52 billion in value in a day. SVB customers asked to withdraw $42 billion of their deposits.

March 10 - Trading in the bank´s shares was suspended. The bank collapsed. The regulator takes control of the bank. It is the third-largest bank failure in U.S. history.

March 12 - Signature Bank, another large bank, fails. The Fed (US central bank) issues measures to prevent the run on the banks from spreading further.

13 March - Bank stocks fall further. There is talk of First Republic collapsing, but it will be rescued in a few days by a group of larger banks. President Joe Biden calms the markets. The Justice Department and the SEC launched investigations into the causes.

15 March - The banking crisis spreads to Europe. Credit Suisse, Deutsche Bank, Société Générale and BNP Paribas stocks fall significantly.

19 March - UBS (Switzerland's largest bank and eternal rival) takes over Credit Suisse for a price of $3.3 billion, but holders of the bank's contingent convertible bonds lose all their money.

De facto, in less than two weeks, an incredible sequence of events has taken place, giving the impression that we are on the verge of a collapse of the banking system.

We Are Unlikely to Get into Big Trouble

Personally, however, I do not think that the events of March will escalate into the financial crisis of 2008. This is due to the specific nature of the current problem.

SVB had a large portion of deposits from the startup and venture environment, which is currently suffering from a lack of capital and a drop in valuation. Therefore, high withdrawals by their clients were natural. It is only the fault of the bank's risk management that they did not properly hedge their positions. It financed long-term investments with short-term funds.

Credit Suisse had been on the edge long before its collapse. As Warren Buffet says: "Only when the tide goes out do you learn who has been swimming naked."

Unlike in 2008, bank balance sheets are healthier. They are holding more high-quality securities on their books with a high probability of repayment, whose prices are only temporarily hammered by the sharp rise in interest rates. Banks' assets have improved markedly compared to 2008 and the equity to liabilities ratio is significantly higher (banks are operating with much less leverage after the last financial crisis).

In terms of capital adequacy, European banks are doing very well, unlike US banks. While in Europe up to 2 200 banks meet strict capital adequacy criteria, in America there are only 14 large banks considered systemically important (too big to fail).

At the same time, regulators have learned very well from the crisis of 15 years ago and know how to react relatively quickly, which has so far been confirmed especially in America.

To be fair, it is also worth mentioning the risks. Even after a slight calming down, the situation could still escalate again. A negative development may occur in the event of escalating deposit withdrawals, the so-called 'bank run' (a massive panic withdrawal of money from banks). Further, banks may be harmed by a continued slump in bonds caused by further interest rate rises or increased loan default rates. All of this has the potential to add fuel to the fire.

Everything Bad Can Be Good for Something

However, this news may also have a good effect on the future state of the economy. At the end of a crisis, the whip always cracks the hardest, and investor emotions are extremely exaggerated. The events of the last few days may accelerate the economic downturn, the credit squeeze, and the associated slowdown in inflation. This would mean the end of the policy of raising interest rates, potentially leading to their gradual easing.

This is one of the reasons for the relatively stable markets. The above-mentioned events have not led to a significant fall in stock indices around the world. Few of us would have predicted that equities would be in the green from the start of the year practically a few days after the collapse of several major banks.

What Are The Risks of Keeping Money in the Bank?

Personally, I think the risk of keeping money in the bank is not high. Compared to a stockbroker, however, there is one big difference that most people don't realize.

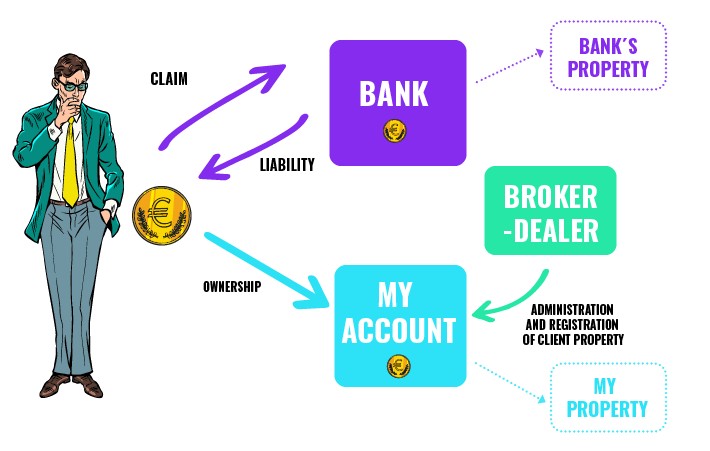

The money you deposit in the bank becomes the property of the bank, and the amount you see as the balance in your checking account is just your claim against the bank. The bank is your debtor and you are its creditor. The bank continues to use your money for its activities, investments, or lending. If the bank should fail and go bankrupt, it will take your money with it.

If the bank's assets (buildings, investments, loans, equipment, and other things) can be monetized, you may be able to get some of your deposits. The money deposited in banks is therefore very sensitive, and in the event of an imminent bank collapse or just negative news, everyone tries to withdraw all their deposits, thus hastening the bank's collapse.

On the other hand, as a securities trader, we manage money separately from our company assets. The money you deposit into your Finax account does not enter our balance sheet. There is no change of ownership. At all times, you remain the owner of both the deposits and the securities we purchase with your account funds. We just keep a record of them for you and manage your investments.

All of the assets we manage, both money and securities, are held in separate segregated accounts that are designated as "Finax Clients". Should Finax go bankrupt, nothing will happen to your assets as they are separate from the trader's assets. The broker's problems cannot be covered by someone else's assets, i.e. not even client assets.

Think of it like a land registry. Finax, like the land registry, only keeps records of the property. While the registry records who owns the flat, we record who owns the shares. If the registry goes bankrupt, you still remain the owner of the apartment.

The State Protects People

Every country wants its economy to thrive and banks are an essential part of that - they are the lifeblood of the economy. The state has an interest in making the banking system run like clockwork. That's why it has issued strict rules that banks must follow and also created the Deposit Protection Fund, which is guaranteed by the state and secures household deposits in the event of a bank failure.

Bank failures in our region are rare, but not impossible. We have only recently seen the example of Sberbank in the Czech Republic, which collapsed in 2022, as clients began to withdraw money from it in droves following the Russian invasion of Ukraine and the imposition of sanctions on Russian banks.

In Slovakia, as across the EU, household deposits in banks are protected up to EUR 100 000 by the Deposit Protection Fund, and the majority of the population can do so peacefully. Those with more money should beware.

In the case of securities traders, there is another protection - the Investment Guarantee Fund. However, this pays compensation for unavailable client assets, i.e. in the event that the trader's employees embezzle (steal) money or the institutions where the trader keeps his money go bankrupt.

This is a fundamental difference from banks. With banks, we are talking about bankruptcy, whereas with traders we are talking about theft. Bankruptcy is more likely, which is why the Investment Guarantee Fund only pays compensation up to EUR 50 000.

The question may arise here as to what happens to my money in Finax if the bank where Finax has an account goes bust. These funds are also covered by the protection of the Investment Guarantee Fund.

At the same time, I must stress that we do not keep much cash in the bank for our clients. They only have money in their accounts between when we receive their payment and when it is invested.

Subsequently, only a maximum of 1.5% of the account value is held in cash to cover the regular portfolio management fee (for no client does this amount currently exceeds 50 000 euros).

This cash is also spread across 5 banks within Central Europe (Tatra banka, Česká spořitelna, BNP Paribas, Raiffeisen Bank, and OTP bank) and property accounts with the custodian.

Which Information Was Omitted in the Flood of News

Finally, let me clarify one piece of information that many bank customers have missed. Credit Suisse contingent convertible bond holders lost all their money. Banks issue these bonds to meet regulatory capital requirements. In the event of a large fall in capital adequacy, these convertible bonds are converted into bank shares or their holders lose their money altogether.

You will also encounter these bonds in Slovakia. They are called MREL bonds or Tier-1 bonds (AT1 or CoCos). Banks refer to them as safe bonds, but in the event of a capital shortage they can be converted into equity in the company (the holders get shares in the financial institution) or they can be liquidated for nothing, so investors can lose their entire investment.

If the issuing bank gets into trouble, e.g. its equity starts to fall, it needs to raise equity capital and there is no interest in issuing new shares, these bonds are the first to go.

So check that you have not invested in these bonds. As I mentioned, I don't expect problems for Slovak banks, but consider whether the yield on these bonds is adequate for the risk being taken.

What to Do if You Are Afraid to Keep Your Money in the Bank

I sleep soundly. I keep a minimum amount of money in the bank for the long term, because it would just be lying around anyway. My money works (is invested) in a Finax account, so I don't have to deal with that problem.

If you don't want to "lend" the money to the bank, it's better to lend it to the government, as they have more credit than the banks. For example, through a bond ETF you can lend money to a few dozen states at once and get a good rate of interest for it.

Create an account and start investing today

The difference in risk is substantial. With a bond ETF, you also get diversification, similar liquidity, and better returns. Currently, government bonds offer a return of 3 to 4% per year, while you typically get nothing in a checking account at the bank.

The "bank run" does not threaten securities dealers. You can withdraw money from them at any time. It's your money, your property, being available to you at all times. If the withdrawals cause the dealers to lose their returns, they will go bankrupt, but you will not lose your assets.

The bank, on the other hand, works with your money; it does not have all the deposits immediately available. Therefore, it also bears liquidity risk. Any bank will be put down if a large percentage of its depositors decide to withdraw their money, as was the case with SVB.

As I have shown and explained, the banks' problems in no way threaten your assets in Finax. On the contrary, holding assets directly in investments is considerably safer in such a specific event, both due to the huge diversification and the direct ownership of securities.

The only impact of events in the banking sector has manifested itself in the share prices of the banks themselves. The most likely scenario, according to Finax, remains the isolation of problems in individual banks. We do not expect contagion to spread, although further turbulence and casualties cannot be ruled out, given the concerns of lenders and bank customers.

At the same time, the collapses of specific institutions represent the culmination of the current cycle and the approaching end of a phase that can safely be described as a lighter banking crisis. In the future, we will all look back on past events as an investment opportunities, just as we look back today on 2020, 2011, 2008, or 2001.