Difficulty

Difficulty

Consumption is a modern phenomenon. I often feel that no matter how much a person earns, he or she is still able to spend their entire monthly income. Not only on essential expenses, but more so to spoil themselves with new clothes, electronics, eating out at restaurants, going on vacations and so on.

I also had a period in my life when I was earning several thousand euros a month, yet my bank balance at the end of the month stayed the same. My consumption grew hand in hand with my income. The higher my salary was, the more exotic holidays I went on, the more expensive things I bought, and at the end my bank balance did not increase.

For many of our clients this situation is something unimaginable, but surveys show that almost a third of Slovaks live paycheck to paycheck without having an emergency fund. Moreover, due to the pandemic, many people found themselves in this exact situation. Others’ already difficult situation had even worsened and many went even further into debt.

Enough is enough! Are you tired of living like this and are you determined to change it? I'll show you the way and where to start. The journey is straightforward, but it is not easy. There are no shortcuts that will magically make you rich.

After Sunny Days Comes the Rain

As long as life goes on as usual, the household can mostly cope with the expenses. You can live off your income, as you are used to this way of life. You know approximately how much you can spend on food; you know that you will go on holiday in the summer, that you will need to buy a few presents for Christmas. Life is beautiful when it is predictable.

But after sunny days, rain will come. Sometimes it's just a drizzle, other times it's a continuous rainfall, but once in a while there is such a downpour that the river spills over. The employer lays off or simply fires you. Your car breaks down, your washing machine breaks down, you or your relatives suddenly fall ill and you have to take care of them. An unexpected pregnancy, or perhaps a tragedy in the family.

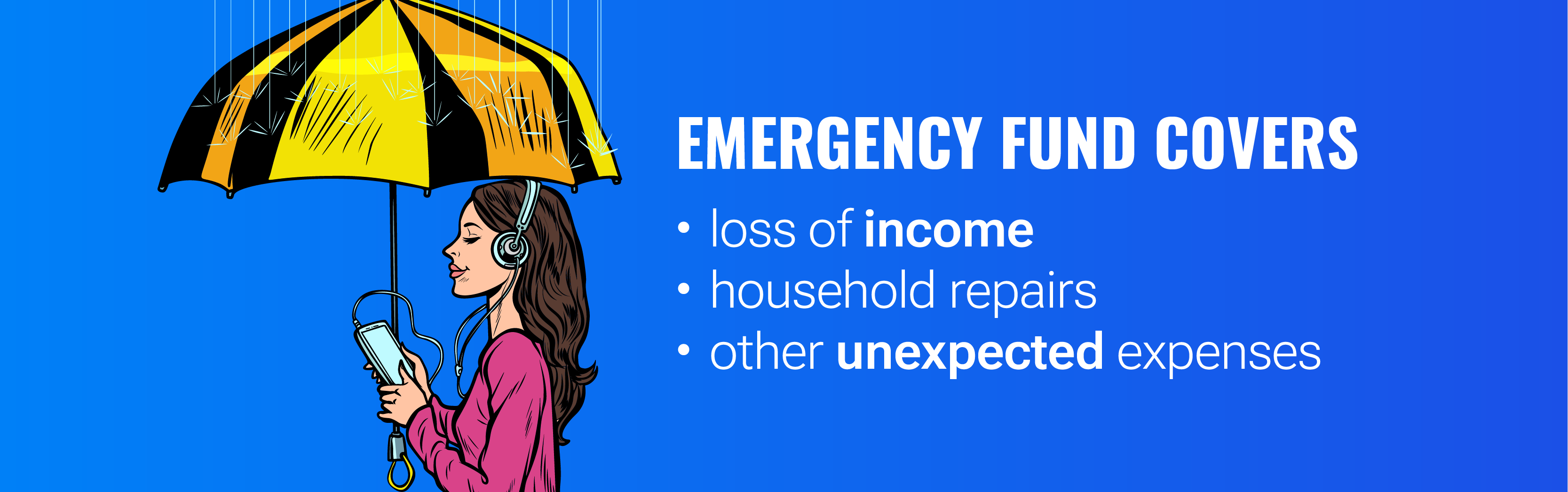

Life is unpredictable, so it is important to be prepared for the unexpected. In fact, the vast majority of families get into financial difficulties because of events that they did not expect and that require their immediate attention. Oftentimes, there are also considerable expenses associated with these events.

Your bank balance is showing a zero and you need a new washing machine. The store will happily sell you the washing machine on an installment plan and the endless cycle of debt begins. If you don't change something in your life, it will start raining again soon. This time the car will give up on you and you are forced to take out a consumer loan from a non-bank institution. The debts pile up and the stack is only getting bigger until the debt gets out of hand.

Save € 500 as Soon as Possible. Create an Emergency Fund.

If you don’t want to get wet, you will need an umbrella. Your first step is to quickly save up 500 euros. You'll build up an emergency fund that will protect you from showers and light rain. Your "umbrella" may not protect you from flooding, but you won't get wet every time and you'll have room to slowly raise your permanent floodwall - a fully funded financial reserve.

We have a very nice saying in Slovakia. A poor man's pot will boil over. People abroad are probably more familiar with Murphy's Laws, named after the aeronautical engineer who used to say: "Whatever can go wrong, will go wrong." Or you might have heard "If you are feeling good, calm down, it will go away."

I know many families that feel like Murphy was a member of their household. Things often go wrong or unforeseen events happen, requiring immediate money outlays. However, I have discovered one thing during my career. Murphy is not friends with people who are financially prepared for unforeseen events.

The moment my bank account balance started to move away from zero, I stopped having the "why me" feelings. Well-known American author Dave Ramsey declared that emergency fund is like a repellent for Murphy's Laws.😊

Create an account and start investing today

To get your family finances under control, start with an emergency fund. € 500 is just a taste of what's to come in the future. A small umbrella. If your household's net income is above € 20,000 a year, increase this amount to € 1,000. After all, you are in a different income bracket and your more expensive car or appliances may be more expensive to repair.

Be Creative, but Save Fast

How am I supposed to build up an emergency fund when I'm living paycheck to paycheck? Be creative. Think of something, but do it quickly. Speed plays a big part in this case. Success is what will motivate in the next steps. After all, your emergency fund is just the first step to getting control of your finances.

One of the reasons why I didn't become a professional tennis player, unlike my brother, was that while he either won the tournament or was at least in the finals in the junior categories, I got eliminated in the quarterfinals. His victories motivated him to train even harder, while I was demotivated by the losses and wanted to go hang out with friends instead of training.

If you can build up your emergency fund quickly, tell yourself. "Yes, I did it!" and you'll be hungry for another victory.

Ask for an extra shift at work, deliver pizzas, work at weekends, sell some of your stuff. If you can't wrap your head around it, check out these tips of mine:

- 12 tips on how to save hundreds of euros monthly

- 10 tips on how to reduce your weekly expenses

- 10 daily routines that will help you save money

Households that are better off income-wise could save up for an emergency fund in one month. But even those who are not that well off should be able to do so in two months at most.

What if You Already Have the Money?

Congratulations, set it aside as an emergency fund and keep it in cash. If you have zero in your bank account but have some savings in mutual funds, a third pillar to which you have voluntarily contributed to in the past, building-society savings, unit-linked life insurance, or other financial products, withdraw 500 euros out of them even at the cost of a small fine.

The only thing that counts is cash. As the saying goes: "Cash is king".

Hide Your Emergency Fund

The package has arrived and you don't have the cash to pay for it? It doesn't matter, after all you have your emergency fund stashed away in your drawer. You run over there, pull out 20 euros and pay the courier. You say to yourself that you'll return it back tomorrow.

No, that's not what we agreed upon. I mentioned already that your emergency fund is for emergency purposes only, not for things you can foresee, and certainly not to pay for a delivery.

Don't keep your 500 euros in your regular account, which you can access with your debit card. It would always tempt you to spend it on a shopping spree.

Believe me, if your emergency fund is easily accessible, it will never be safe and you will always have the urge to use it for "non-emergency" purchases. Therefore, you need to store your emergency fund so that it is not in plain sight, but available when you need it.

Ideally, you can use one of the many online banks (I described their fees here), where you open an account just for this purpose, or your bank may also offer a special free savings account. In the event of an emergency, you can withdraw the money or transfer it to your regular bank account.

Do not invest this money. You will use other resources for that later. You should have the money available within 24 hours at latest. No exceptions.

Repay Your Debt Only After You Have Built up an Emergency Fund

If you are in debt and have toxic loans with interest rate (APR) above 5%, it is still a good idea to build up an emergency fund first and only start paying off those debts with extra repayments after. Rain will always come. If you want to get rid of debts, which for most people will be about more than just 500 euros, you first need to be prepared for the rainy days, so that you can fully concentrate on paying them off even when these days come.

Imagine your car breaks down and you have to pay 400 euros to repair it. If you only concentrate on paying off your debt without having an emergency fund, you would have to borrow once again to pay for the car repair.

How would you feel in such a case? You work like crazy to pay off your debts, but you just had to borrow money again. You would feel disappointed, as if you had just lost a game. A match in which you started off well, but the referee’s decision turned the match around, and you ended up losing because of it.

If you've decided to get out of debt, you need to do it for good. Once and for all. Don't allow the loans or Murphy the chance to come back and bite you.

Do Not Confuse Emergencies With Basic Consumption

Caution, never spend your emergency fund on things that you can anticipate in advance and that should be included in your financial plan.

Christmas happens every year. This year it will be on 24.12. and, surprise, surprise, next year it will once again be on 24.12. You go on holiday regularly in the summer. In May, you have to pay your estate tax and in September, the children go to school. And no, not even a 50% discount at Ikea counts as an emergency.

These are not expenses on which you should use your emergency fund. These expenses should be accounted for in your budget. Only use your emergency fund for the things we mentioned above. Layoffs, illness, broken washing machine, these are the things you couldn't foresee and can't pay for out of your budget.

What if There Is an Emergency?

Have you fallen ill and had your salary reduced by €300 due to the illness, being unable to cover this difference from your current budget? It's time to use your emergency fund. You don't have to experience financial stress because you have set up the fund for this very purpose. You have money to take care of it.

However, once you are healthy, you must do everything you can to refill your financial reserve back to €500 as soon as possible. Try to replenish your reserve quickly, as sometimes the rain might be followed by even more rain. If you don't replenish your emergency fund, over time there will be nothing left and Murphy will be at your door.

What if a thunderstorm hits and your emergency fund won’t be able to cover all of the expenses? First and foremost, remember that by building an emergency fund, the process of getting control of your money is just in the beginning, and in the next steps you'll be building a fully funded financial reserve that you can draw from in the event of a major expense.

If you have not yet built up an emergency fund, or if you may be in the process of building one, try to avoid increasing your debt at all costs. If it's just a washing machine, try doing laundry at your parents' house for a few weekends. If it's a car, dust off the bike or use public transport. Be creative and find other ways of dealing with the situation without incurring additional debt.

I Have a 500-Euro Emergency Fund, Now What?

You have managed to successfully build up an emergency fund of 500 euros. Congratulations, you've taken your first big step towards financial freedom and you're probably hungry for another victory.

If you are in debt, the next step should be to pay off any outstanding toxic loans. We will cover this topic in a future blog. However, in the meantime, you can check out Janči's webinar on Good and Bad Debt.

If you are not in debt, you can fully focus on building up a fully funded financial reserve, or also have a look at my last year webinars on how to invest your full financial reserve.

Good luck!